Summary

- After depreciating nearly 80% in the last 5 years, TripAdvisor’s stock seems to have hit the bottom and has all the chances to appreciate in the near future.

- With 463 million MAUs and one of the largest libraries of travel-related content on the web, TripAdvisor will continue to be an important player in the online travel industry.

- By having a positive net cash position and attractive growth prospects, TripAdvisor will be able to create value in the foreseeable future, as travel rebounds.

After depreciating nearly 80% in the last 5 years, TripAdvisor’s (TRIP) stock seems to have hit the bottom and has all the chances to appreciate in the near future, as there’s an indication that the travel industry slowly starts to recover. While in the past TripAdvisor failed to unlock value despite being one of the most popular travel websites on Earth, it has been able to constantly generate a positive FCF and its current cash reserves outweigh the company’s total debt. At the same time, with more than 460 million monthly active users, TripAdvisor could be viewed as a potential takeover target by major OTAs and tech companies, which have plans to establish a stronger presence in the online travel niche.

Even though the company will be unprofitable this year due to the pandemic, the analysts estimate that TripAdvisor will return to profitability in 2021. Considering that the stock trades close to its all-time low, I decided to purchase the company’s shares, as I believe that the recovery of travel and the potential acquisition in the future will drive TripAdvisor’s stock higher in months to come.

Recovery On Its Way

The spread of COVID-19 all around the globe disrupted TripAdvisor’s business. As a company that heavily relies on the growth of the tourism industry, TripAdvisor suffered immense losses in the first half of the year. Over the years, the company’s earnings were fluctuating from time to time as a result of poor governance, but in the first three months of the current year, it had probably the worst performance in its history. In Q1, TripAdvisor’s revenues declined by 26.1% Y/Y to $278 million, while profit during the period fell by 161% Y/Y to a net loss of $16 million.

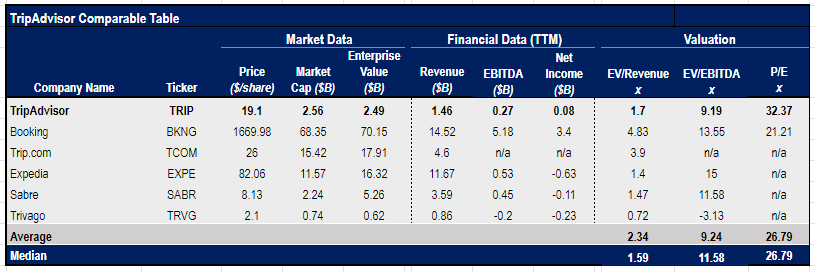

However, TripAdvisor is not the only company among its peers that showed a poor performance due to the pandemic. The table below shows that lots of companies had similar results and are not profitable anymore. Only Booking (BKNG) along with TripAdvisor has been profitable on a TTM basis and has a positive P/E ratio. With EV/EBITDA of 9.19x, TripAdvisor could be considered undervalued compared to its peers, as the industry’s median EV/EBITDA is 11.58x. However, considering the uncertain environment in which all the companies from the table operate, a simple comparable analysis is not enough to decide whether it is worth purchasing TripAdvisor shares or not.

Source: Yahoo Finance. The table was created by the author

Online travel is a very competitive niche. Over the years, two major OTAs, Expedia (EXPE) and Booking, have been establishing a greater presence in the industry by acquiring travel-related platforms and services and adding more users to their ecosystems. Currently, both of them form a duopoly in the OTA field, which benefits both companies. As one of the biggest travel websites in the world, TripAdvisor remains one of the major sources of traffic for those companies. However, the spread of COVID-19 forced them to cut their advertising budgets and preserve as much cash as possible to survive the current crisis. Since the whole travel industry is in disarray right now, TripAdvisor is expected to lose a substantial amount of money this year, as its advertising revenues will decline in 2020. In May, Deutsche Bank (DB) downgraded TripAdvisor due to its high reliance on other companies that use its platform for advertising.

The good news is that TripAdvisor is more than just an advertising and reservation platform. TripAdvisor is first and foremost a community-based platform with social media and online search features, which helps its users to find everything they want about travel. With nearly a billion of reviews and opinions and more than 460 million average monthly users, TripAdvisor can leverage its platform by offering different experiences to travelers. In the last 3 years, the experiences and dining (E&D) business was growing at a compounded annual growth rate of 31% and it currently accounts for 29% of the overall revenues, an increase from 17% in 2017. By pivoting to E&D, TripAdvisor was able to diversify its sources of income and offset some of the declines from its advertising business.