Summary

- Fox showed a strong performance in the last few months, as its advertising and affiliate revenues continue to grow.

- Strong brand awareness, low valuation multiples and a positive outlook for the future are the main reasons why I remain bullish on Fox.

- I continue to hold a long position in Fox.

Fox Corporation (FOXA)(FOX) continues to be a solid media stock that has great potential to create additional shareholder value in the next few quarters. The upcoming Presidential election will help the company to drive its advertising and affiliate revenues and establish a stronger presence in the news business. Despite cord-cutting taking place right now, Fox was not greatly affected by it was able to weather the storm, while its competitors were ruthlessly fighting with each other for their own place under the sun. At the same time, the company continues to be undervalued to its peers and I believe that acquiring its stock at the current market price is a bargain, as there are a number of catalysts that will push the stock higher in the foreseeable future. Overall, I remain bullish on Fox and continue to hold my long position that I opened last Summer.

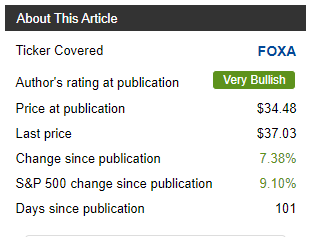

Since the publication of my latest article in November, Fox’s stock has increased by 7%, slowly lagging behind the S&P 500 growth of 9%.

Nevertheless, the company continues to be a conservative media powerhouse with no real competition on a nationwide scale. Since becoming a standalone company earlier last year, Fox was able to build a strong balance sheet and return value in the form of buybacks and dividends, which will be discussed further below. Despite the ongoing cord-cutting, Fox is not under an imminent threat of becoming extinct. The news business, unlike the entertainment business, is somewhat hedged against the current entry of tech companies into the media industry. As a result of this, Fox is able to drive top-line growth, diversify its portfolio of assets and create additional shareholder value, as its major source of income is and will continue to be a news business.

The latest earnings report that was released earlier this month clearly shows that Fox is not under a major threat from any disruptors. In Q2, the company beat analysts’ estimates, as its advertising and affiliate revenues increased by 1.16% and 6.77% to $2.01 billion and $1.44 billion Y/Y, respectively. Even though the company lost some of its subscribers, the higher fee structure helped it to drive growth during the three-month period. Strong brand awareness and the lack of real nationwide competitors that are targeting the same right-leaning conservative audience, is Fox’s major competitive advantage that will help it to weather any upcoming storm.

Despite an outstanding performance in the last few months, Fox continues to trade below its major peers. The chart below shows that only ViacomCBS (VIACA) stock, which I also own, trades below Fox’s stock, while all the other media companies had a better performance in the last 52 weeks.